Geopolitics: In January, for the first time in months, there was little news of market importance to note in the geopolitical domain. However, shortly after the end of the month, reports of a Chinese "weather" balloon flying 60,000 feet over the US, soon to be shot down over the Atlantic, came to surface, disrupting the period of calm. This occurred right when relations between the two countries, which had been tense throughout 2022, seemed to be improving.

Nonetheless, this incident should have no major effect on the markets. As previously noted, Chinese monetary authorities continue to actively provide additional liquidity in order to strengthen the domestic economy and increase consumer demand. Moreover, regulations on domestic tech companies have been eased, and changes made to the IPO rules have been boosting investor confidence and leading to a strong rally in the Shanghai index, contributing to a general risk-on sentiment internationally.

Stock market: The stock market rebounded strongly in January, with the S&P 500 gaining 6.18% during the month, the small cap Russell 2000 up 9.69% and the Nasdaq 100 advancing 10.625%. Overseas markets were equally strong, with the Euro Stoxx 50 index higher by 9.75% and the MSCI EAFE index gaining 6.3%.

Continued good news on the inflation front propelled prices higher as core inflation (YoY) fell to 5.7% in December and the core Personal Consumption Expenditure (PCE) price index, the Fed’s favorite inflation indicator, came in at 4.4%, beneath forecasts. Interest rates fell substantially as a result of the decline and with earnings reports generally coming in around (already reduced) expectations, the market rallied to start the year.

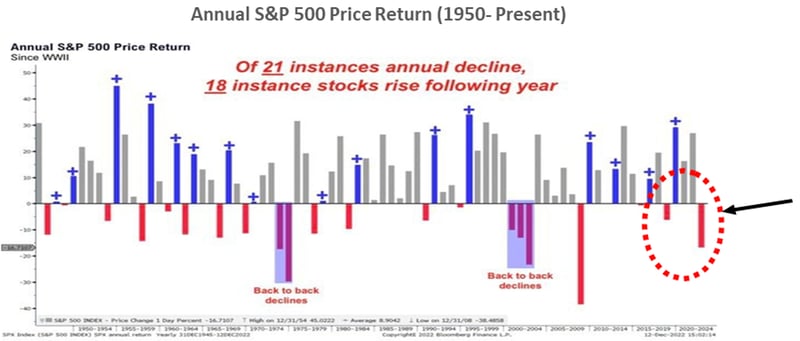

Historically, when the market experiences a bear market of consequence, as it did in 2022, it tends to perform quite well in the following year. Since 1950, there have been 21 instances when the S&P 500 index declined for the calendar year. In 18 of those instances markets advanced the following calendar year, an impressive 85.7% positive rate.

Source: Fundstrat, Bloomberg

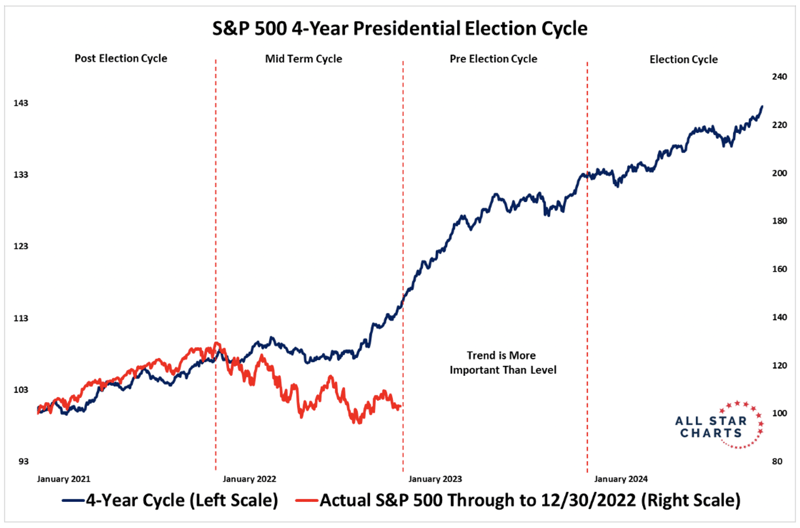

We have commented in the past about the S&P 500’s 4-year Presidential cycle. Historically markets have struggled – relatively speaking – the first two years following a Presidential election as more restrictive economic and tax policies are put in place. Conversely, markets tend to outperform in years 3 and 4 as more stimulative policies are put in place to boost growth as election time nears. The market anticipates this and begins discounting higher future earnings, turning price trends upwards. Whether this year follows the same pattern will depend mightily on how far the Fed goes in tightening monetary policy.

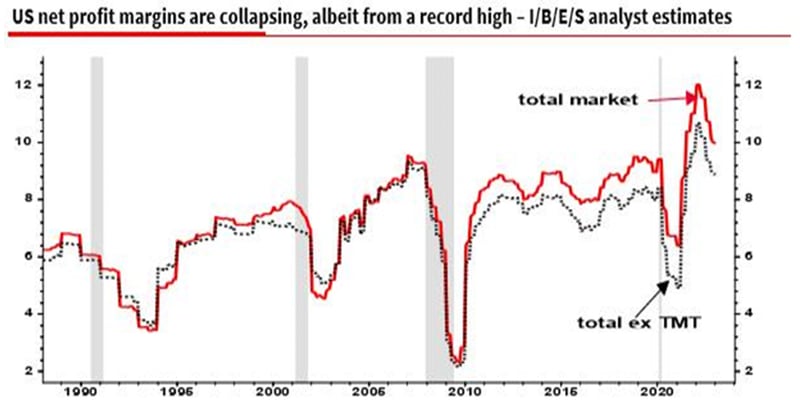

Turning to corporate earnings, there is a bear rationale for why the 2022 market decline isn’t over - we have yet to see the second in a two-step revaluation process. The first step in last year’s re-rating was mainly a function of higher interest rates - the rapid rise in the discount rate translated into substantially lower multiples being applied to corporate earnings. Secondly, even though most of that multiple contraction is likely behind us, we now face the prospect of a steep decline in earnings brought on by a slowing economy and possible recession. As we see below, leading indicators of future corporate earnings growth are already turning over with profit margins eroding. Until the Street gets clarity on these issues, investor confidence will be tentative.

Source: Datastream

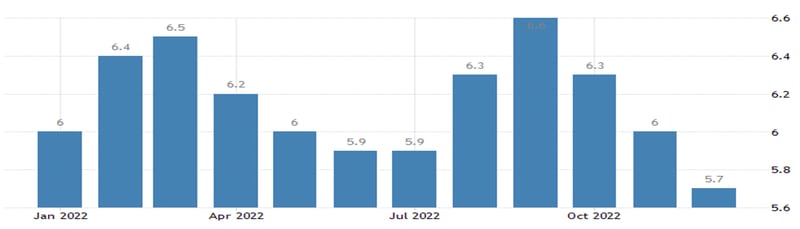

Monetary Policy and the Fed: The chart below shows the recent monthly readings in the YoY change to core CPI.

Tradingeconomics.com | U.S. Bureau of Labor Statistics

Since the peak in September the readings have consistently come in lower than anticipated which has surprised many market observers, particularly as labor markets remain healthy. Unemployment claims, generally viewed as a reliable leading indicator of recessionary conditions, have counterintuitively fallen over the past two months and are nearing cycle lows.

The U.S. JOLTs (Job Openings and Labor Transfer) Index, a measure of overall labor demand, rebounded strongly last month, with the number of job openings in the United States increasing to 11.0 million in December, the most in 5 months and above market expectations of 10.25 million.

Employment statistics are lagging indicators of economic activity and with the numerous (and continuing) layoffs being announced this year, it’s reasonable to expect these numbers to reverse to some degree. For now, the Fed is seeing an economy that has downshifted but still advancing, even as overall price levels recede. The overarching question is how long will this period of disinflation, as Chairman Powell describes it, last and what impact will it have on prices?

One of the most critical indicators of long-term inflationary pressures, labor costs, remain relatively well behaved as wage growth has ticked down recently. While this is a welcome development for the Fed, the absolute level remains elevated and will likely need to come down before Fed policy shifts to being more accommodative.

Bond market: The bond market started the year on a positive note, with bond sectors (government, corporate and mortgage-backed) enjoying strong gains across the board. The 10-year Treasury returned 3.46% in the month, the Corporate Investment Grade index was up 4.01%, the U.S. Mortgage-Backed index rose 3.29% and the High Yield sector gained 3.81%.

Not surprisingly, volatility dropped as prices rallied, a sign perhaps that bond investors’ fears of accelerating inflation and/or imminent recession were overblown and are now receding. Volatility in the bond market generally shows up first in lower quality issues but so far this cycle, high yield bonds have been relatively range bound compared to the damage seen in the Treasury and corporate markets. In fact, spreads to Treasuries have fallen over 200 basis points since peaking in July 2002 and recently fell below the 4% level. This tightening is much more indicative of a healthy economy rather than one entering recession and is difficult to square with an inverted yield curve (2-10 year) at its widest since 1981.

Managed Income Strategy

Entering the year in a Risk-Off posture, Managed Income placed its first Risk-On trade for 2023 in mid-January. The move was initiated as a result of a positive price trend developing in the High Yield fixed income space beginning in late December and a reduction in overall volatility across the fixed income landscape to begin the year. The MOVE Index (ICE BOFA US BOND MARKET OPTION VOL INDEX), often considered the bond equivalent to the VIX, decreased by more than 40% since October 2022 as bond volatility subsided. With this Risk-On move the Portfolio Management Team elected for a diversified bond allocation, investing across High Yield, Floating Rate and Investment Grade Corporate fixed income securities.

Dynamic Growth Strategy

Dynamic Growth entered into its first Risk-on position in late January as the month was coming to a close. Despite the strong start in equities to begin the year, Dynamic Growth remained defensive through much of the month as intraweek volatility remained elevated in equity markets, leading the Strategy to a more cautious posture. The breakout in equities in mid-January saw the S&P 500 break through its 200-day moving average and the long-term resistance trend line that began in early 2022. This strength was reflective of the Risk-On signal generated by the Dynamic Growth decision model. Given elevated intraday volatility and relative market uncertainty, we anticipate the Strategy may pivot between Risk-On and Risk-Off more frequently in the coming weeks than historical norms.

Active Advantage Strategy

The Active Advantage Strategy also started the year in a fully Risk-Off posture, before pivoting in mid-January, making a partial portfolio allocation to the High Yield fixed income category. As January drew to a close the Strategy added a small allocation to equities to complement the High Yield exposure, while still maintaining a partial cash allocation. As with Dynamic Growth, we anticipate allocations within Active Advantage will likely see continued allocation adjustments to both equity and fixed income securities in the coming months as the Strategy risk pivots through choppy markets.