Geopolitics: Russia continues to make gradual progress on the ground in Ukraine while simultaneously pressing its strategic advantage as a significant energy supplier to Europe. The Nord Stream 1 pipeline - the major delivery route to Europe for Russian gas and majority owned by Gazprom – is now delivering only 20% of its total capacity to the EU with Russia threatening to reduce supplies even further. Such a cutback threatens to force wholesale reductions in industrial production in the EU and particularly in Germany, as the continent struggles to replenish gas supplies for the coming winter.

On the other side of the globe, tensions have ratcheted up between China and the U.S. as a result of Congresswoman Nancy Pelosi’s visit to Asia. Chairman Xi strongly warned the U.S. that a visit to Taiwan by Ms. Pelosi would constitute a major provocation and result in serious consequences for the West. Given the hugely important role both China and Taiwan play in the semiconductor industry, any potential military confrontation holds potentially grave consequences for the global economy. The pivotal role China and Taiwan play is the primary reason Congress passed the “Chips and Science” act in July, which will provide approximately $52 billion in government subsidies to encourage domestic chip production / R&D. The passage is another example of the ongoing reshoring of supply chains globally, a trend expected to continue in the years ahead as countries work to ensure supply of critical components.

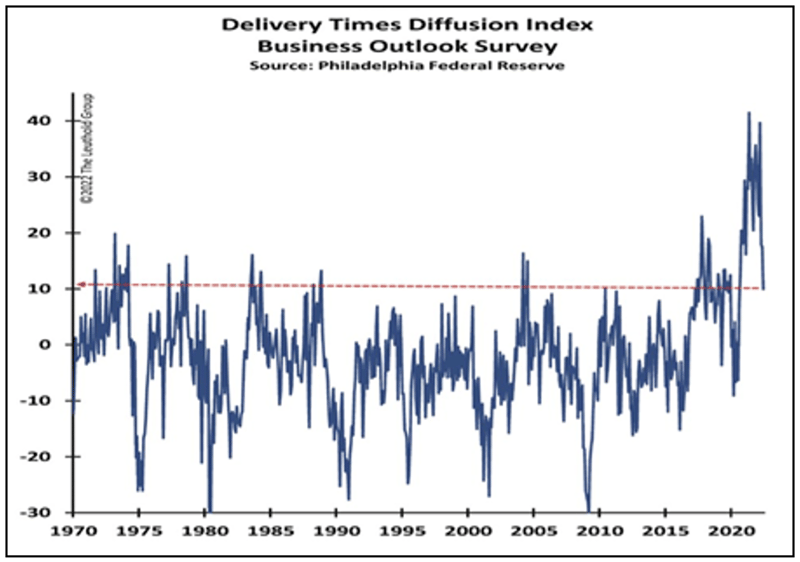

On the topic of supply chains, there has been substantial improvement in delivery times as evidenced in this graph from the Philadelphia Federal Reserve. The shrinking of lead times will help to reduce price pressures and represents, at least for now, a welcome return to some semblance of normality.

Stock Market: The stock market rebounded strongly in July, posting its best gain since November 2020. For the month, the S&P 500 Index advanced 9.22%, while the Nasdaq 100 Index jumped 12.60% and the small cap Russell 2000 was up 10.44%. The positive returns stood in marked contrast to the prior two months and were driven mainly by a perceived dampening in the Federal Reserve’s hawkish outlook for inflation. This, combined with extremely negative investor sentiment, indicates inflation may be peaking, and better than expected earnings reports and underinvested institutions provided the spark that resulted in a rally off the mid-month lows.

Whether this is a new bull or merely a bear market rally is top of mind for investors. Bullish investors believe the current economic slowdown will be shallow based on still healthy consumer and corporate balance sheets, demand that is slowing but not crashing, historically extreme investor sentiment and accompanying low equity exposure, robust corporate demand for shares, and a relatively benign interest rate environment. The recent fall in the dollar has also added an important tailwind to corporate profits, although the durability of the move is still in question.

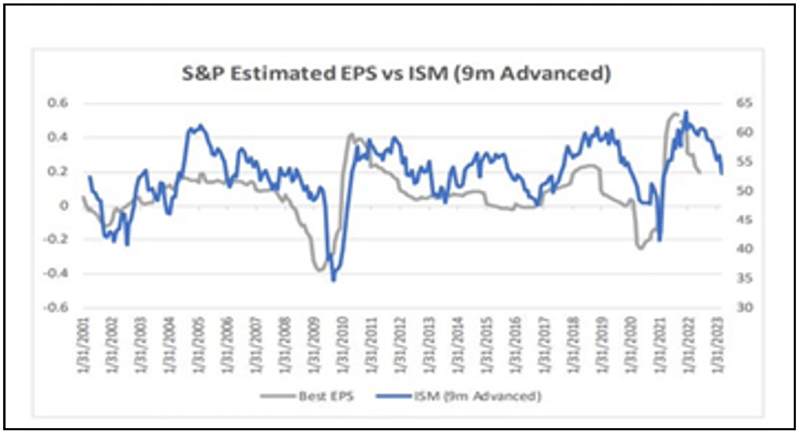

Bearish investors on the other hand argue the negative effects of the Fed’s tightening have barely begun, earnings projections are far too optimistic, the 2-10 year yield curve remains inverted – historically a precursor to recession - and valuations are elevated from a historical perspective. With regards to corporate earnings, leading indicators such as the Institute of Supply Management PMI reports suggest weaker earnings ahead (see chart), while the breadth of downward revisions has accelerated and isn’t yet reflected in analyst forecasts. Although nominal revenue and profits are boosted by high inflation, profits adjusted for inflation are likely to be squeezed in the months ahead as margins shrink.

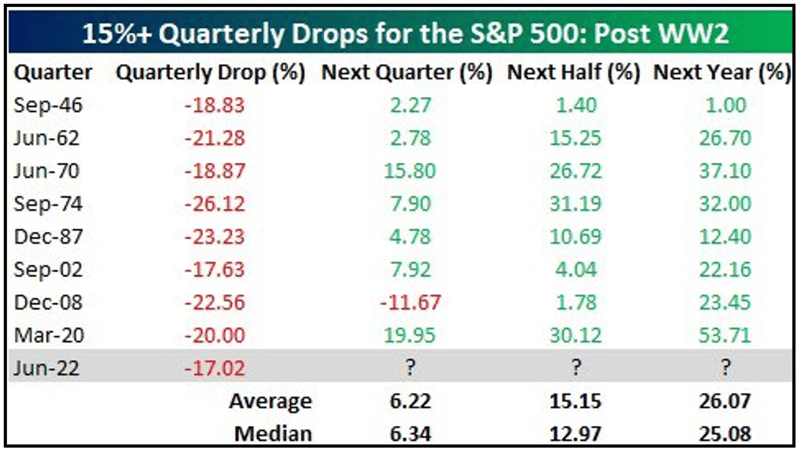

Source: Cantor Fitzgerald, L.P.

Turning to post World War II history for guidance, whenever the S&P 500 Index has suffered a quarterly decline of greater than 15%, the exception being the Great Financial Crisis in 2008 - 9, the Index has rebounded strongly over the next 3, 6 and 12 months with the average annual gain in excess of 26%.

Source: Bespoke Investment Group

In the short term, however, we are entering the two seasonally worst months of the year (25-year look back). Much in the coming months will depend on the course of inflation, of course, and the success of the Fed’s efforts to slow the economy without something “breaking” (financial market crisis or a deep recession).

Bond Market: Bond indices saw solid gains throughout, led by lower grade indices. High yield bonds advanced 5.90% in the month while investment grade bonds advanced 3.24%. Government bonds also rallied strongly from mid-month onwards, with 10-year yields falling nearly 44 basis points to end the month at 2.64%. Credit spreads contracted dramatically in July, moving in tandem with stocks as investor risk appetite moved higher. The tightening wasn’t uniform, as high yield spreads moved far more than investment grade (17% vs 7%), with IG yield spreads closing the month at 1.53.

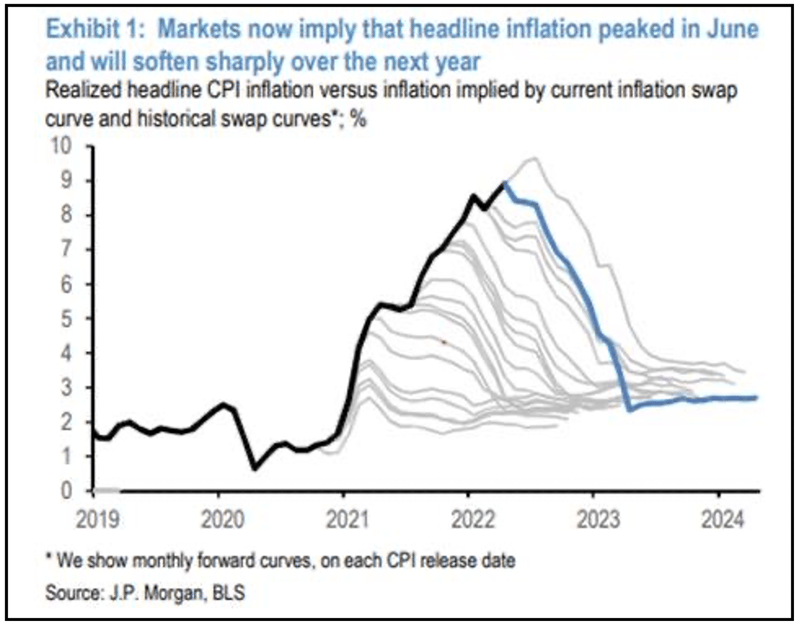

The fall in yields and spread compression may be a sign of reduced inflation fears, with more investors believing inflation has peaked (see chart below) with the June Consumer Price Index (“CPI”) print of 9.1% marking the high for this cycle. Setting aside the technical question of whether the U.S. economy is in recession, it’s clear that economic activity has slowed, particularly in the housing sector where June existing home sales declined by - 5.4% from May and -14.2% from a year ago. Pending home sales were down -20% year over year.

Monetary Policy and the Federal Reserve: The Federal Reserve’s FOMC raised the Fed Funds rate by the widely anticipated 75 basis points, bringing the rate to 2.50%. Investors took heart in Chairman Powell’s comments when he expressly noted there were signs of a slowing economy and future actions would be data dependent, which market participants took to mean the Fed was prepared to pivot to a less aggressive hiking regime sooner rather than later. Others, including several Federal Reserve governors, argue that investors may be getting ahead of themselves as the Fed remains steadfast in its efforts to bring long-term inflation to its targeted 2 - 3%.

Bank lending is growing at the fastest pace since the Great Financial Crisis (ex-Covid surge), putting real money in consumer pockets. Unemployment remains historically low and ECI wages ran a hot 1.4% YoY in the second quarter of 2022. All this suggests a Fed Pivot may be a way off.

Managed Income Strategy: The Managed Income Strategy entered a Risk-On trade in mid-July, marking its second such trade in 2022. Positive price trends began developing in the high yield bond category at the beginning of the month as spreads narrowed from a high of 5.99 on July 7th to 4.83 at the end of the month, as measured by the ICE BofA US High Yield Index Option-Adjusted Spread, pushing prices higher. During this same period, volatility in the fixed income market began to subside, with the ICE BofAML U.S. Bond Market Option Volatility Index (“Move Index”) decreasing by approximately 25% throughout July. While volatility in fixed income is still elevated by historical standards, the trend is encouraging, and we’ll continue to monitor if the current positive price trend can sustain further.

Dynamic Growth Strategy: The Dynamic Growth Strategy also entered a Risk-On trade in July, trading into equities at the beginning of the month. Despite longer-term negative price trends in the stock market, the strategy was able to identify an entry point early in the month to take advantage of the recent market surge. As was the case in fixed income, volatility in the equity market subsided throughout July as the U.S. stock market moved higher, with the Chicago Board Options Exchange's CBOE Volatility Index (“VIX”) closing July at 21.33, its lowest level since April 20th.

Active Advantage Strategy: Our latest strategy, Active Advantage, is a tactical balanced strategy integrating both our equity and fixed income approaches into an offering able to shift allocations across multiple markets simultaneously. Active Advantage ended the second quarter defensively positioned in a Risk-Off posture. Throughout July the strategy shifted its allocation, initially making a small equity allocation before shifting to its “base” portfolio, allocated 60% to equities and 40% to fixed income, where it remained positioned through the end of the month.

In the case of all three strategies, we are encouraged by recent gains but remain cautious given the longer-term negative trend across both stocks and bonds. We will continue to rely upon our model signals to navigate these markets, maintaining our primary objective of providing steady, above average positive returns with low volatility and downside protection.