Few investors have had the intestinal fortitude to remain resolutely invested throughout the

numerous crises (and associated temporary market dips) that have marked the long-term bull

market that began in 2009. This time it’s the threat of a coronavirus pandemic emanating from

China which has quickly spread across the globe. This new virus has many similarities to SARS, which

surfaced in November 2002 and remained a threat until July 2003. SARS killed 774 people and

infected 8,098 persons in 29 countries.

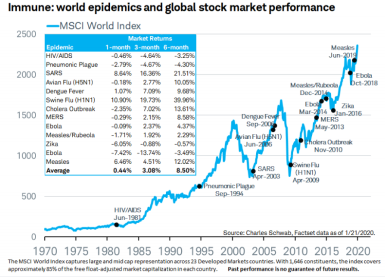

It’s too early to tell what the ultimate outcome of the current outbreak will be, but it might help to

review a timeline of past epidemics from 1970 to see how the market has reacted historically. What

we see from the chart below is there is little correlation between the outbreak of these diseases and

downside reversals in price trend of the market. Of course, these diseases were all eventually

brought under control so none of them were sufficiently severe and long-lasting to impact long-term

global economic growth. Nonetheless, the clear lesson to be learned is if one had been scared out

of a fully invested position in response to these outbreaks, returns would have suffered in nearly

every instance and sometimes dramatically so.

This illustrates one reason why Kensington doesn’t attempt to factor global macroeconomic or

geopolitical risks into its model metrics. The underlying assumption that guides our models is that

supply and demand ultimately determine price movement and that shifts in the balance between

the two can be measured mathematically. We don’t try to ascertain what the actual forces are that

drive the balance at a given moment. In fact, we believe it’s impossible to know those factors.

Instead, we focus our efforts on the practical management and execution of our time-tested

methodology. When our model indicates buyers are dominating sellers, the Managed Income

strategy knows to be fully invested in high-yield corporate bonds. When the model indicates sellers

have begun to take control and we are moving into a risk-off environment, the portfolio is shifted

into low risk Treasury securities.

Our strategy takes a practical approach to geopolitical matters. This means that rather than making

investment decisions based on fears of potential global pandemics, we stick to the facts. With this in

mind, our strategy seeks to provide consistent, attractive returns despite tumultuous current

events, and to minimize downside exposure in adverse market environments.