Market Insights is a weekly piece in which Kensington’s Portfolio Management team will share interesting and thought-provoking charts that we believe provide insight into markets and the current investment landscape.

As market participants wait for what has been the most widely predicted recession in US history, let’s evaluate why a recession may or may not occur in 2023 and the implications for the market if it does.

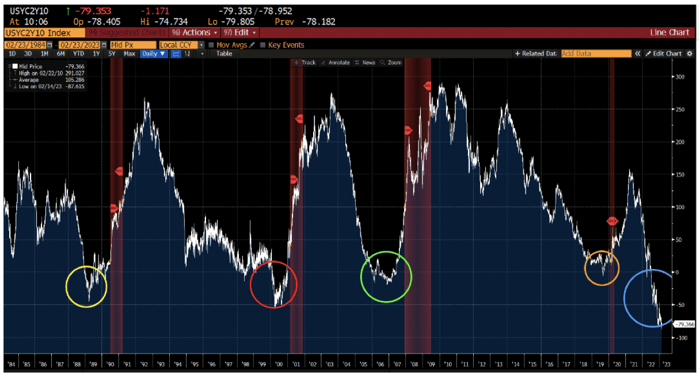

One of the most widely sourced predictors for impending recessions in the US is the inversion of 2-year and 10-year Treasury yield curve. When the curve inverts (meaning the 2yr yield is higher than the 10yr yield), there has been a better than two-thirds chance of a recession at some point in the next year and a greater than 98% chance of a recession at some point in the next two years, according to Bespoke.

The chart below shows the 2-year and 10-year curve, with the red bars indicating past recessions and the circles showing when we've seen the curve invert. Interestingly, it is typically the reversal of the inversion that seems to be predictive of a recession, as opposed to the inversion itself.

Source: tradingview.com

So where do we stand now? As we approach the one-year anniversary of the initial inversion this cycle, which first occurred in late March 2022, the inversion recently hit its widest margin since the early 1980s reaching a level of -0.87% on Monday, February 27th. While the inversion had seemed to bottom out over the past month around -0.79%, recent upside surprises to inflation have pushed the inversion deeper.

This Time It's Different?

Source: BLS, Bloomberg

While yield curve inversion has been a strong predictor of past recessions, there are some that feel this time it’s different. Those four words are often referred to as the “most dangerous four words in investing”, but this time the doubter is the actual inventor of the yield curve indicator, Campbell Harvey, finance professor at Duke University. In an interview with MarketWatch, Professor Harvey points to a number of factors that may be playing into why the spread's powers of forecasting may be off. Adjusting the yields for inflation shows that the curves are flat for the 2-year and 10-year curve, and positive for the 3-month and 10-year curve (shown above), another widely sourced indicator of an impending recession. Harvey points to strong labor demand and housing resiliency as other factors that may indicate a false signal for the indicator.

Whether this time is different or not, investors need to be nimble for the possibility of a recession and further market downturn. The average S&P 500 drawdown during a recession is 31.5%, dating back to 1957. The ability to sidestep or at least limit these types of potential drawdowns could be the difference in an investor's ability to achieve their financial goals.

Forward-looking statements are based on management’s then current views and assumptions and, as a result, are subject to certain risks and uncertainties that could cause actual results to differ materially from those projected. This market insight is for informational purposes only and should not be construed as a solicitation to buy or sell, or to invest in any investment product or strategy. Investing involves risk including loss of principal.

Click below to subscribe to our Insights!

Receive email notifications when new articles are published