2021 year-end summary points:

- The Economy: The U.S. economy experienced a strong expansion throughout 2021, with consensus estimates of real GDP growth to end near 5% for the year. Even as the threat of new COVID-19 variants arose, consumer demand and job growth remained resilient and finished strong, with consumer spending expected to rise by 5.3% and unemployment to fall to 4.3% for Q4.

- Inflation: With the surge in economic growth and consumer demand came higher than average inflation. It was to be expected, especially in the first half of the year with the base-effect and lingering issues with pandemic-related supply chain disruptions. For the most part, the Federal Reserve initially framed inflation as transitory, but as the year ended it became clear that the supply chain disruptions and inflationary pressures were going to be longer-lasting than expected. By November, year-over-year CPI had reached 6.8%, its highest since 1982.

- Monetary Policy: Monetary policy was highly accommodative for most of the year, in continuation from 2020. However, as inflationary pressures persisted, the Federal Reserve was forced to change its stance toward the end of the year, with Fed Chair Powell announcing that it was “a good time to retire” the term “transitory”. Following that announcement came indications that the tapering of bond purchases would need to be accelerated and could end as early as March 2022.

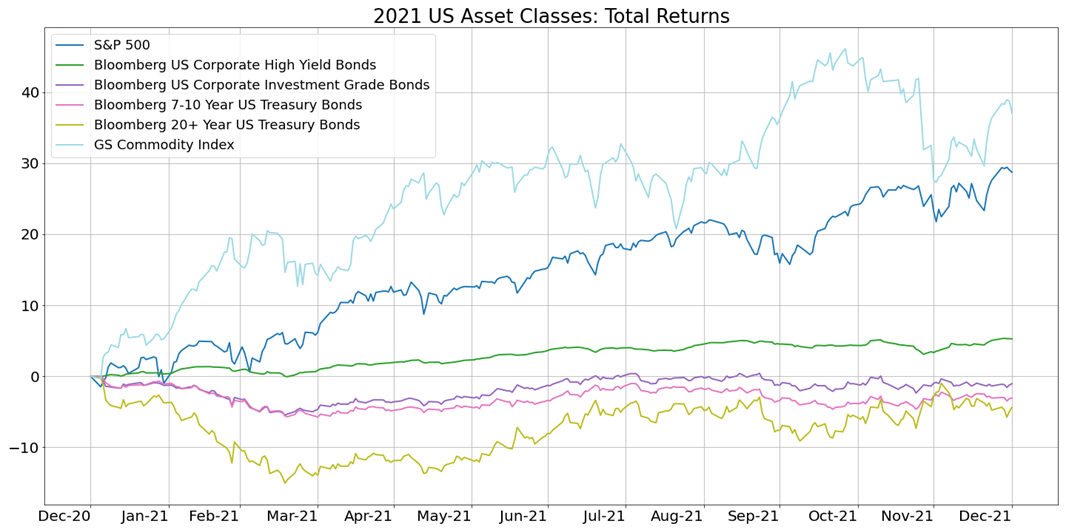

- Asset Class Performance: On the heels of strong economic growth and inflation, equities and commodities led the way in returns for the year. The S&P 500 rose 28.7% and the Goldman Sachs Commodity Index advanced about 37%. Fixed income saw lackluster performance, as a taper tantrum at the beginning of the year and Fed hawkishness toward the end provided headwinds for duration-sensitive assets. One of the few areas in fixed income that still finished positive in 2021 was high yield bonds, which are more sensitive to default risk than interest rate movements.

Figure 1. Data from Bloomberg Financial LP. Calculations performed by Kensington Asset Management.

Managed Income Strategy

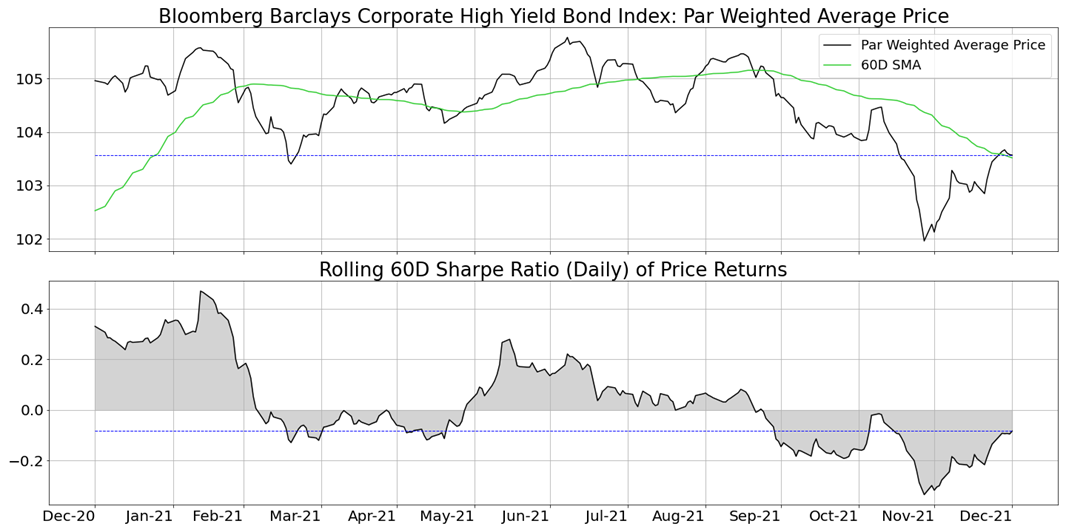

Throughout 2021, default rates in high yield debt remained low, and it’s expected by most credit rating agencies that this would continue into 2022. As a result, high yield bonds have been trading at premiums not seen since 2014, which suggests limited potential for price appreciation. Most of 2021’s return for the asset class was attributable to the coupon component. As can be seen in Figure 2, high yield bond prices started trending negatively in Q3 as Fed policy shifted to a more hawkish stance. Despite a modest rebound in December, high yield prices still sit lower relative to their high point in 2021 and are just touching their 60-day1 moving average, while their risk-adjusted price returns for the same period continue to remain negative. As mentioned in last month’s commentary, our Managed Income strategy shifted to a risk-off posture in late November and remains that way coming into the new year. While our trend following systems do not utilize the indicators mentioned above, they help illustrate the utility of trend following in this asset class for risk management purposes.

Figure 2. Data from Bloomberg Professional L.P. Calculations performed by Kensington Asset Management.

Dynamic Growth Strategy

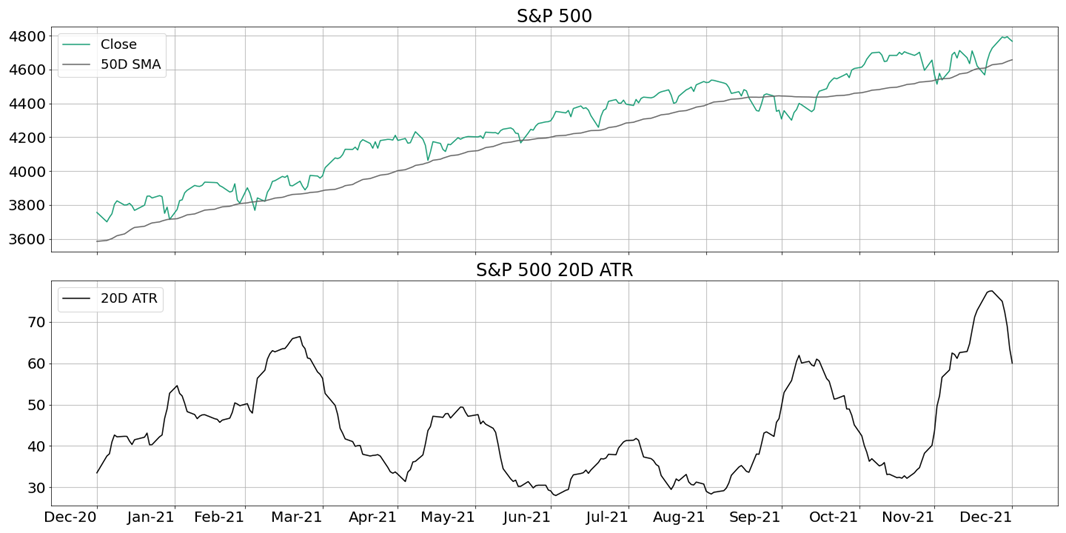

Despite the market tremors that occurred in November, calendar effects prevailed in December with major U.S. equity indices finishing positive for the month. As we discussed in our previous article at the end of November, the S&P 500 was at a major technical and psychological junction, having fallen to its 50-day moving average; this was a level where investors have reflexively "bought the dip" throughout the year. However, as we can see in the expansion of trading ranges as measured by Average True Range2 in the bottom panel of Figure 3, doing so at that point was a lot riskier relative to buying the dip during the summer months, when liquidity was more abundant. As with our Managed Income strategy, our Dynamic Growth strategy remained in a risk-off posture through the end of the year. As we enter the new year, we will continue to monitor model signals for a potential re-entry point.

Figure 3. Data from Norgate Data. Calculations performed by Kensington Asset Management.

Kensington Asset Management

Under the current uncertain economic conditions and in light of the Federal Reserve’s hawkish stance, we believe that an active approach to investing in the market is more important than ever. At the same time, we recognize the potential psychological pitfalls that can occur in an active approach when markets become adversarial and wide swinging. With that in mind, we have and always will strictly adhere to our disciplined model-driven process to manage risk in these challenging market environments. For 2022, we hope to continue to capture trends when they occur, while attempting to mitigate drawdowns in times of stress, and appreciate our clients’ trust in us to do so.

Best regards,

Kensington Asset Management Team