Market Insights is a piece in which Kensington’s Portfolio Management team will share interesting and thought-provoking charts that we believe provide insight into markets and the current investment landscape.

Yields on the Rise

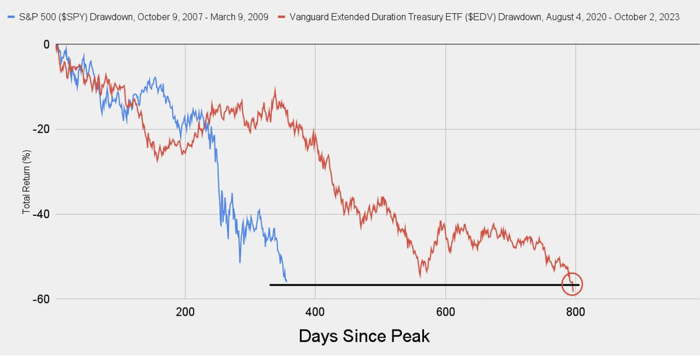

This week we’ve witnessed a stunning rise in longer-term Treasury yields (and drop in prices), with the 30-year bond briefly hitting an effective yield of 5% Wednesday morning, the first such occurrence in 16 years. The consequent decline in bond prices, which commenced in 2020 but has been primarily driven by the Federal Reserve's rate-hiking cycle starting in 2022, is now accelerating, resulting in a drawdown in long-duration US Treasuries worse than the drawdown stocks experienced during the 2008 financial crisis (see chart below).

Total Drawdown in Ultra Long-Duration U.S. Treasury Bonds Now Exceeds Stock

Market Peak-to-Trough Stock Market Crash During Great Financial Crisis

Several factors have contributed to this precipitous drop. Last year, we witnessed a sharp rise in shorter-duration Treasuries, consistent with the Fed Funds rate moving higher. This year, we are seeing the longer end of the curve rise, driven by the anticipation that rates will remain elevated for an extended period, as emphasized by the Fed during their September Federal Open Market Committee (“FOMC”) meeting. However, other factors are at play as well. One primary consideration is the diminishing foreign demand from buyers like China, which now holds $493 billion less in US Treasuries than it did at its peak in 2013/2014 (see chart below).

China: US Treasury Holdings

(USD Billions)

Source: Bloomberg: Tavi Costa | ©2023 Crescat Capital

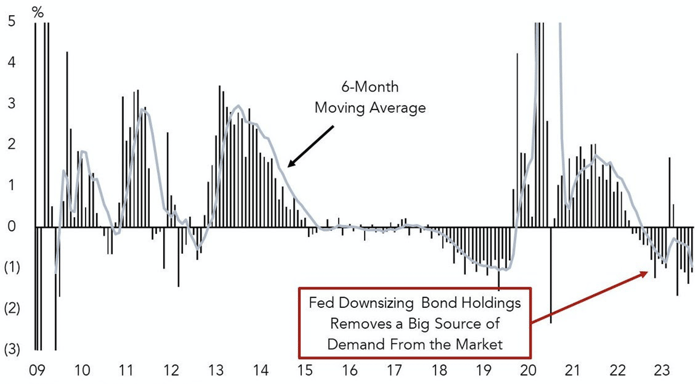

Another significant player in the treasury market, the Federal Reserve, is not only refraining from purchasing but is also actively reducing its holdings of Treasuries (see chart below), further impacting overall demand.

Month-Over-Month Change in the Federal Reserve's Balance Sheet

Date: 2009 Through September 20, 2023

Source: Federal Reserve Board, Game of Trades

Based on monthly average of weekly balance sheet levels

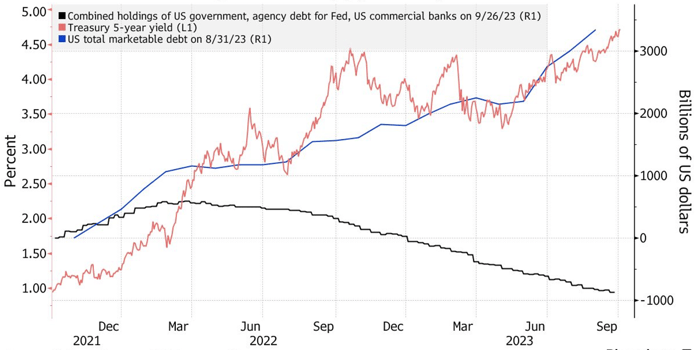

This lack of demand coincides with a surge in supply, creating a vicious cycle. Yields continue to rise because the US Treasury needs to issue a significant amount of debt beyond their initial plan. They are compelled to do so because higher yields have led to escalating interest payments on the existing debt. Consequently, they must issue even more debt, which, in turn, causes yields to rise even higher, resulting in even larger interest payments and the need for more debt issuance. This cycle persists at a time when both domestic and international demand is waning (see chart below).

US Yields March Higher as Suppy Rises, Demand Wavers

Source: Federal Reserve, US Treasure, Bloomberg

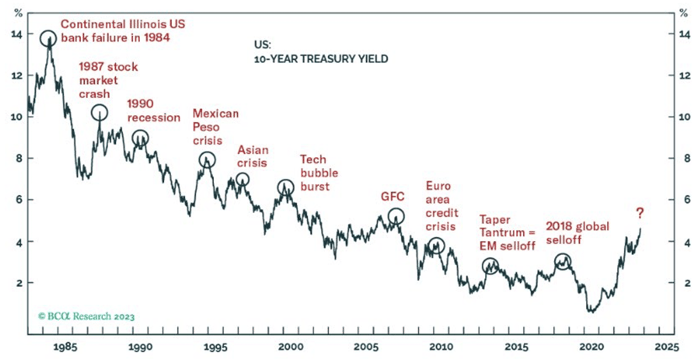

Historically, bond bear markets usually end in response to a financial crisis which forces the Fed to reverse course and aggressively reduce rates in order to restore stability. The chart below clearly shows the history of this process since 1985.

A Rise in Bond Yields Typically Ends with a Financial Accident

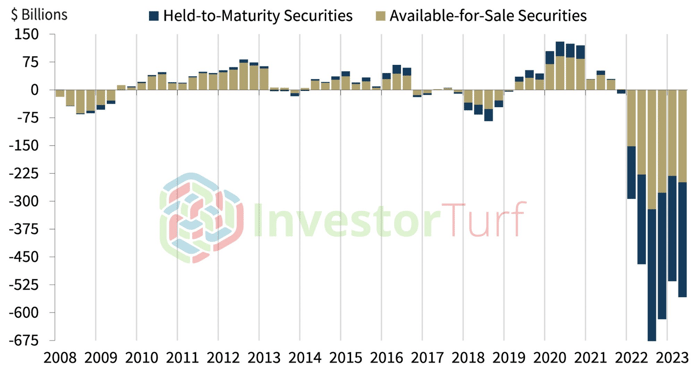

So far, to the amazement of many, the dramatic rise in rates since 2020 has not precipitated a crisis. Nevertheless, several sectors of the economy could be potential catalysts for a financial “accident.” We've previously discussed the mounting risks in real estate and the banking sector. The banking sector, in particular, faces increased risks as rates continue to climb. Even before the recent surge in rates, banks were carrying nearly $558 billion in unrealized losses through Q2 (see chart below). It's worth noting that the total unrealized losses have decreased by $131 billion since their peak in Q3 2022, partly due to the collapse of three banks with substantial unrealized losses, causing their balance sheets to disappear from the system. It's likely that these unrealized losses have increased significantly by the end of Q3, adding further pressure on an industry that has witnessed significant deposit outflows over the past year.

Unrealized Gains (Losses) on Investment Securities

Source: FDIC

If yields remain at current levels or continue to rise, it will be intriguing to hear what the Federal Reserve will have to say at its next FOMC meeting, scheduled for October 31st. This week, Treasury Secretary Janet Yellen seemed to cast doubt on the idea of rates remaining elevated for an extended period, stating that it was “by no means a given.” As we’ve been emphasizing in recent Market Insights, the only certainty is that something must change because the interest rate environment, even before this week’s surge in yields, is likely to be unsustainable in the long term.

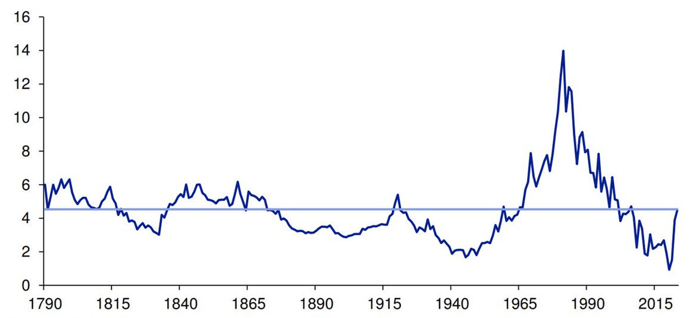

On the other hand, perhaps our viewpoint is clouded by recency bias. As a country, we’ve grown accustomed to near zero rates for three decades, but as the chart below illustrates, the recent surge in rates has only brought us back to the historical average for US Treasury rates dating back to the late 18th century.

10yr US Government Yields Back to Average for the First Time Since 2007

Source: GFD, Deutsche Bank

Regardless, if rates do remain elevated, or average as the chart above implies, challenges are likely to surface in certain corners of the market that have grown overly reliant on cheap borrowing costs. While this may result in market disruptions, history has shown us that disruptions in market behavior usually present significant investment opportunities for those who are agile enough to successfully navigate them.

Forward-looking statements are based on management’s then current views and assumptions and, as a result, are subject to certain risks and uncertainties that could cause actual results to differ materially from those projected. This market insight is for informational purposes only and should not be construed as a solicitation to buy or sell, or to invest in any investment product or strategy. Investing involves risk including loss of principal.

Click below to subscribe to our Insights!

Receive email notifications when new articles are published