In February 2023 we laid out the case for Dynamic Growth as a core equity allocation predicated on how incorporating investments with low correlation to the market (and each other) may benefit portfolio performance and provide true portfolio diversification. In this Brief, we will provide similar analysis for the Kensington Managed Income Strategy and demonstrate how utilizing Managed Income as a core component of a diversified bond portfolio may be advantageous, particularly in a rapidly changing market landscape.

A Case for Core Fixed Income

Investors use Managed Income in various places within an overall fixed income allocation. One of the challenges in identifying its most appropriate place is that it doesn’t fit neatly into most investor’s predefined fixed income boxes. Rather, its tactical nature allows it to shift its characteristics to best suit the prevailing market.

Given the Strategy’s focus on higher yielding fixed income, some utilize it as a high yield fund. Others, given its unique Risk-On/Risk-Off methodology, choose to view it as an “alternative” or non-traditional bond allocation. While all portfolios are unique, and Managed Income may be utilized as a high yield or alternative allocation, we believe that a more appropriate allocation for the Strategy is as a core fixed income investment, complementing existing passive allocations at the centerpiece of the portfolio.

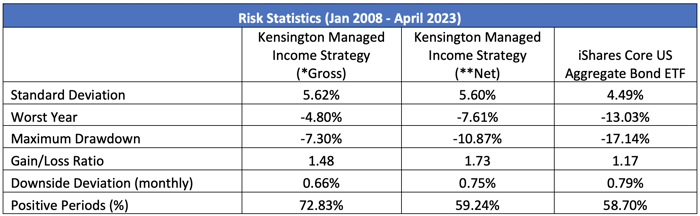

One of the primary reasons for this is that Managed Income, despite investing in securities that would typically not be considered “core” fixed income assets, has demonstrated over time a risk profile in line (or better) with bond offerings often used for the core piece of bond portfolios. Let’s evaluate a series of risk statistics for Managed Income versus the iShares Core US Aggregate Bond ETF (ticker: AGG), which we’ll use as a proxy for a traditional core allocation:

Source: Morningstar

Kensington Asset Management does not charge an advisory fee.

*Gross returns do not include the deduction of transaction costs and are shown as supplemental information.

**Net 3% performance is shown because 3% is the generally assumed highest model wrap fee.

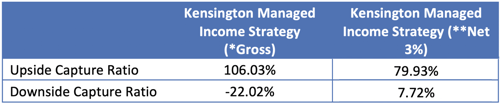

Managed Income outperforms in virtually every risk category despite its typical allocation to higher yielding fixed income. One of the ways the Strategy has been able to accomplish this is by operating on a Risk-On and Risk-Off basis, shifting its portfolio offensively and defensively based on Kensington’s quantitative assessment of the market opportunity, positive or negative. The objective of this methodology is to identify and participate in rising markets and shift defensively when our quantitative system determines there is weakness in the market, with the goal of sidestepping volatility and avoiding drawdowns. This is perhaps best illustrated by evaluating the Strategy’s upside and downside capture ratios, which determines how much the Strategy participates in the upward and downward movement of its stated benchmark. For Managed Income, that benchmark is the Bloomberg U.S. Aggregate Bond Index, a proxy often utilized for core fixed income, as we did above.

Source: Morningstar

Kensington Asset Management does not charge an advisory fee.

*Gross returns do not include the deduction of transaction costs and are shown as supplemental information.

**Net 3% performance is shown because 3% is the generally assumed highest model wrap fee.

Historically, Managed Income has participated in over 100% of the Aggregate Bond Index upward movement, while primarily avoiding the benchmark’s downside movement. In short, the Strategy acts more like a core fixed income strategy when you want it to (upside) and less so when you don’t want it to (downside).

Asset Correlation

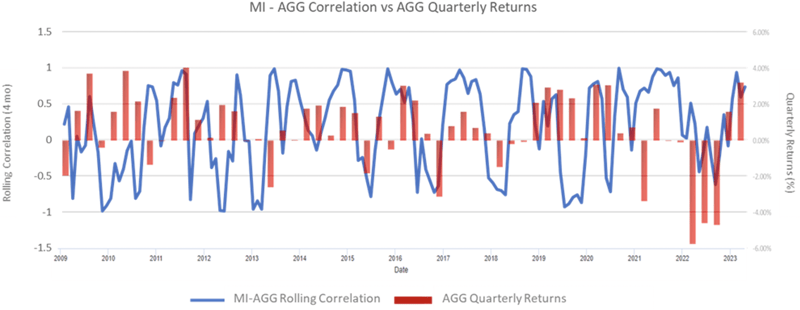

The cornerstone of portfolio diversification is the ability to identify and utilize assets with low correlation to each other. As you would expect from the data above, Managed Income maintains a low correlation to the Aggregate Bond Index at 0.26 since inception, which is a key consideration for pairing it with more traditional core holdings. One aspect of correlation that is often overlooked, however, is that correlations are not static. Often during periods of market stress, traditional investments that would typically show low/lower correlation to each other see an increase in correlation, reducing portfolio diversification when it is most needed.

This again is where Managed Income’s Risk-On/Risk-Off system can be additive for portfolio construction. As seen in the chart below, the correlation between Managed Income and the Aggregate Bond Index is adaptive based on portfolio positioning and can seek to demonstrate high correlation to the Index when the market is deemed to be strong and low correlation when the market is deemed to be vulnerable.

Source: Portfolio Visualizer and Kensington Asset Management. Correlation is calculated on a 4-month rolling basis.

Differing Rate Environments

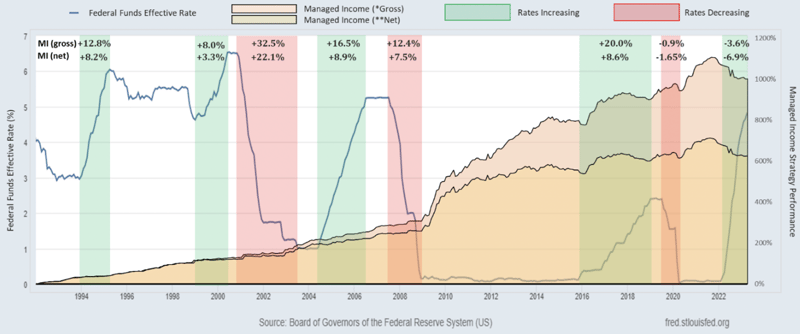

Another key aspect to evaluate when determining what will make up the core of your fixed income portfolio, particularly in today’s ever changing rate environment, is how the investment performs during differing rate regimes, both rising and falling. If we evaluate the last 8 time periods in which the Federal Reserve meaningfully increased or decreased the Federal Funds rate (below), we see that Managed Income has performed admirably in both rising and falling rate environments.

Source: Board of Governors of the Federal Reserve System (US), Morningstar and Kensington Asset Management

Kensington Asset Management does not charge an advisory fee.

*Gross returns do not include the deduction of transaction costs and are shown as supplemental information.

**Net 3% performance is shown because 3% is the generally assumed highest model wrap fee.

Portfolio Impact – Diversifying the Core

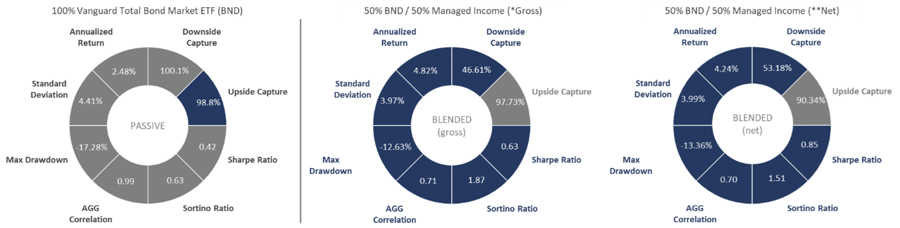

Ultimately, we believe the most important factor when evaluating a new investment for portfolios, and where they fit in a portfolio, is what impact it has on the overall asset allocation in terms of portfolio risk and return. So, let’s evaluate how Managed Income impacts a portfolio when utilized as a complement to an otherwise diversified fixed income portfolio. For this analysis we will use the Vanguard Total Bond Market ETF (Ticker: BND) as a proxy for an overall US fixed income allocation, as the ETF spans across the fixed income spectrum. Comparing a portfolio made up solely of BND versus a portfolio split evenly between BND and Managed Income for the period January 2008 to March 2023 yields the following results across numerous portfolio statistics:

Source: Portfolio Visualizer

Kensington Asset Management does not charge an advisory fee.

*Gross returns do not include the deduction of transaction costs and are shown as supplemental information.

**Net 3% performance is shown because 3% is the generally assumed highest model wrap fee.

The Blended Portfolio, which incorporates both a passive (BND) and active (Managed Income) strategy has historically outperformed the 100% passive portfolio (BND) in virtually every statistical category including annualized return, standard deviation, max drawdown and each of the risk adjusted return metrics (Sharpe, Sortino). It is for this reason we believe utilizing Managed Income as a complement to existing core bond allocations makes sense for most investors. Managed Income’s tactical approach offers a unique and compelling solution to pair with traditional passive fixed income securities to better diversify fixed income portfolios across an ever-changing fixed income environment.

This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact the professional advisor of their choosing.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Kensington Asset Management, LLC (“KAM”). No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by KAM or any other person. While such sources are believed to be reliable, KAM does not assume any responsibility for the accuracy or completeness of such information. KAM does not undertake any obligation to update the information contained herein as of any future date.

There is no guarantee that the investment objectives will be achieved. Moreover, the past performance is not a guarantee or indicator of future results.

Investing in securities involves risk, including loss of principal. The risks associated with this Strategy include general market risk, credit risk, interest rate risk or risk of the portfolio not performing as expected.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy. For example, a strategy may typically hold substantially fewer securities than are contained in an index.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.